Market cools during what is usually the busiest time of year

What's happening in Spanish Fort, Daphne and Fairhope: July 2025

By Janet English

The current Eastern Shore housing market is in a cooling-off period.

Inventory is increasing in Daphne, Fairhope and Spanish Fort, which can count 644 single-family homes for sale, at this writing. This will lead to longer marketing times, as evidenced by the absorption rate (how long it takes to sell every listed home compared to the rate of sales).

Daphne, Ala., has 4 months of inventory

n Spanish Fort, Ala., has 4.05 months of inventory

n Fairhope, Ala., has 5.23.

Meanwhile, the median sales price has declined.

The average sales price has declined, as well, dropping $64,000 since March.

The two trends may also show that buyers are adjusting their sights to lower-priced homes to offset interest rates hovering just under 7%.

This information comes from a Baldwin County Multiple Listing Service data analysis, as well as reports from the Realtors’ Property Resource, often known as the RPR.

Interestingly, the RPR still narrowly pegs Spanish Fort and Daphne as sellers’ markets, while putting Fairhope almost into the category of a balanced market, where neither buyer nor seller have the advantage.

Another stat to pay attention to is how much sellers take off their list price in order to sell. For Eastern Shore builders, it’s only 0.5%, while owners of existing homes have lately sliced off 3.2% to close.

On to the numbers ....

Eastern Shore 2nd Quarter stats:

Number of homes sold

2024 2025

581 614

Average sales price

$497,899 $486,878

Price decrease to close

2.5% 2.2%

Spanish Fort:

Number of homes sold:

2024 2025

118 129

Average sales price:

$423,712 $447,352

Price decrease to close

1.45% 1.8%

Daphne:

Number of homes sold

2024 2025

206 236

Average sales price:

$399,406 $389,749

Price decrease to close

2.4% 2%

Fairhope:

Number of homes sold:

2024 2025

257 247

Average sales price:

$610,910 $600,323

Price decrease to close

2.9% 3.25%

Home prices rose, but sales plunged in 2023 in Daphne, Spanish Fort and Fairhope.

Expect lower mortage rates this year

There’s something happening here … what it is, ain’t exactly clear – “For What It’s Worth,” Buffalo Springfield.

For the second year in a row, home prices rose but the number of sales fell dramatically.

Two factors are in a tug-o-war both locally and nationally: (1) A new generation entering the home-buying market is creating a high interest in properties, but (2) The rapid increases in mortgage interest rates are, obviously, giving many buyers pause.

The good news is that specialists in the industry believe that rates will fall to 6% by year’s end and maybe go as low as 5.3%. Meanwhile, a whole segment of the population is delaying moves, holding on to that 2.8% interest rate that they locked in a few years ago.

On the Eastern Shore of the Mobile, Ala., metro area, the number of sales in 2023 tumbled 22% --1,976 sales vs. 2,551 sales in 2022. (In 2022, sales dropped 13% from the previous year.) Nonetheless, the average sales price in 2023 climbed 9% on the heels of rising 16% in 2022. The average sales price in 2023 was $479,406.

New construction, which represents 30% of all home sales, continues to prop up the market in Spanish Fort, Daphne and Fairhope. One example that illustrates this is how much sellers took off their list prices in 2023 in order to sell. For owners of existing homes, it was 3.38%. For builders, who seemed to have a nice pool of potential buyers, it was only 0.24%. But builders were, and are, offering great mortgage rate incentives, with rates well below the going average.

On to the numbers:

| |

|

Number of homes sold

Eastern Shore:

2022 2023

2551 1976

Average sales price:

$450,176 $479,406

Price decrease to close

1.5% 1.8%

Spanish Fort:

Number of homes sold:

2022 2023

504 377

Average sales price:

$406,915 $419,685

Price decrease to close

0.6% 1.8%

|

|

|

|

| |

|

Daphne:

Number of homes sold

2022 2023

1135 752

Average sales price:

$358,596 $369,578

Price decrease to close

0.7% 1.73%

Fairhope:

Number of homes sold:

2022 2023

912 847

Average sales price:

$588,057 $603,499

Price decrease to close

2.4% 2.94%

|

|

Sept 2022 Housing Report Daphne, Fairhope, Spanish Fort

The signs of a moderating housing market were on full display in September in Spanish Fort, Daphne and Fairhope.

Average single-family sales prices fell 10% on the Eastern Shore of Mobile, Ala. This drop was so precipitous I ran the numbers twice using MLS data from both September and August. The decline was despite the sales of seven $1 million-plus homes, which can skew the data upward.

While the ebb and flow of pricing changes with what’s selling at any given time, there’s no doubt that mortgage interest rates nearing 7% has sent shock waves through the entire U.S. home market.

Another telling sign: Sellers took on average 4% off list price to sell. In previous months, that number has been around 2%. In a stable, balanced market the magic number is 3%.

And the number of homes going under contract also fell 16%.

So, it may get a little rocky out there but remember this:

n Home prices have increased 28% on the Eastern Shore since January 2020.

n People will have to buy and people will have to sell. Life, work, family situations all change and with it the need to move remains.

n Finally, our inventory remains exceptionally low.

On to the numbers:

Eastern Shore Single-Family Homes for sale:

Exactly where we were this time in September with 330 for sale, holding steady with 328 the first week of August and 315 in early July.

Spanish Fort homes for sale: 54

Daphne homes for sale: 121

Fairhope homes for sale: 155

Pending sales:

Total: 277, down from 331 in early September, 352 in early August and 379 in July.

Spanish Fort: 46

Daphne: 136

Fairhope: 95

Closed sales for September 2022:

Total: 196, down from 215 in August, 243 in July and 238 in June.

Average sales price: $429,612, down from $479,872 in August, $485,383 in July and $464,788 in June.

Median sales price: $383,980, steady from $390,000 in August, $388,500 in July and $380,000 in June.

List-to-sale percentage: 96%, which is off from 98.1% in September, 97.9% in July and 98.85% in June.

September home sales by town:

Spanish Fort: 53

Daphne: 77

Fairhope: 66

The number of homes for sale on the Eastern Shore of Mobile Bay fell to new lows in January, and this is worth taking a deeper look into what’s happening.

There are 172 active single-family homes – many of them under construction and not move-in ready – in Spanish Fort, Daphne and Fairhope. The falling number of available homes has been attributed to this area being a hot-spot for growth over the last decade.

Meanwhile, other forces were at work. Sure, there is the pandemic and subsequent shortages of labor and materials. But it’s more than that.

From a recent article by CNBC’s Diana Olick:

“The U.S. is short 5.24 million homes, an increase of 1.4 million from the 2019 gap of 3.84 million, according to new research from Realtor.com.

The U.S. Census found that 12.3 million American households were formed from January 2012 to June 2021, but just 7 million new single-family homes were built during that time.”

This bolsters the argument that this market is not a bubble that’s going to burst anytime soon, according to many economists and analysts in the real estate and building industries.

That said, there could be other events that swing the market one way or another. For example, the Great Recession cut the housing market off at its knees; and the Pandemic, weirdly, ignited it.

On to the numbers:

Eastern Shore Single-Family Homes for sale:

172, down from 218 in early January.

Spanish Fort homes for sale: 25

Daphne homes for sale: 60

Fairhope homes for sale: 87

Pending sales:

Total: 486, up from 432 in early January.

Spanish Fort: 100

Daphne: 227

Fairhope: 159

Closed sales for January 2022:

Total: 202, down from 245 in December.

Average sales price: $404,672, up from $401, 589 in December and $395,912 in November.

Median sales price: $345,000, down from $365,900 in November.

List-to-sale percentage: 98.3%, virtually unchanged over the last three months.

December’s home sales by town:

Spanish Fort: 26

Daphne: 85

Fairhope: 78

September 2021 homes sales report

Home sales in Spanish Fort, Daphne and Fairhope ticked up in September. But the real eye-popping number is that the average sales price on the Eastern Shore jumped from $387,092 in August to $452,290 in September.

The number is real … and so were the 14 sales of $1-million-plus properties on the Eastern Shore in September that radically skewed that statistic. The highest priced sale was for bay front house near the Grand Hotel in Point Clear with 4,568 square feet, built in 1920. It sold for $4,850,000. Cash.

So no, your home and my home didn’t just appreciate some $60,000 in one month. Sorry.

On to the numbers:

Eastern Shore Homes for sale:

302, little changed from 308 the second week of September, but up from 248 in early August.

Spanish Fort homes for sale: 46

Daphne homes for sale: 100

Fairhope homes for sale: 156

Pending sales:

Total: 484, down from 506 the second week of September and 520 in early August.

Spanish Fort: 85

Daphne: 219

Fairhope: 180

Closed sales for September 2021:

Total: 268, up from 239 in August but lower than July’s 287.

Average sales price: $452,290, up from $387,092 in August and $397,858 in July.

Median sales price: $324,970, down from August’s $345,000 and little changed from $323,900 in July.

List-to-sale percentage: 98.8%, little changed from August’s 98.8%.

September’s home sales by town:

Spanish Fort: 48

Daphne: 123

Fairhope: 97

March 2021 Market report for Spanish Fort, Daphne and Fairhope

Housing inventory continues to shrink with just 210 single-family homes available for purchase in Spanish Fort, Daphne and Fairhope in this first full week of April.

For years and years, this market easily had 1,200 homes for sale at any given time.

The shortage of homes nationwide is largely the result of the Pandemic, which led to a host of shortages in goods and services worldwide. Hopefully, the situation will ease before further damaging the economy

On to the numbers:

Eastern Shore Homes for sale: 210, down from 245 in February and 313 in January

Spanish Fort homes for sale: 47

Daphne homes for sale: 61

Fairhope homes for sale: 102

Pending sales:

Total: 584, up again from 541 the first of March and 455 in early February.

Spanish Fort: 124

Daphne: 271

Fairhope: 189

Closed sales for March 2021:

Total: 267, up from 193, up from 156 in January, but trailing 236 in December.

Average sales price: $358,632, down from $366,086 in February but up from $350,038 in January.

Median sales price: $311,595, down from $326,000 in February but also up from $279,452 in January.

List-to-sale percentage: Tightened up to 98.7% from 97.7%.

March home sales by town:

Spanish Fort: 63

Daphne: 109

Fairhope: 95

Somethings happening here ...

What it is ain't exactly clear -- Buffalo Springfield's "For What It's Worth"

Homes sales shot up 18 percent!

Sales prices rose 6.2 percent!

It took only 71 days, on average, from list to contract! And if the house were priced right, just a handful of days might have passed.

Those are some of the eye-catching numbers from the third quarter of 2020 here on the Eastern Shore.

It's a great time to SELL!!!

Here’s another truth. Some buyers are being priced out of this market. There is too much demand, too little supply. Prices are climbing to the point that the average sales price of a home on the Eastern Shore in this third quarter was $347,010.

Lawrence Yun, the chief economist for the National Association of Realtors, says the following:

"A mix of surging buyer demand and low inventory puts the industry in uncharted territory. The [national] median home price has soared to an all-time high of $300,000, threatening to ‘choke off’ first-time buyers from the market and depress the national homeownership rate.”

"Uncharted territory" is a phrase best associated with B-movie character actors piloting a starship off into the next nebula. When associated with real estate, it's a term that can give one pause.

Then again, hasn’t ALL of 2020 been uncharted territory? So let’s dig into some more details about third-quarter sales:

Eastern Shore as a whole: 752 homes sold during the quarter, compared to 633 in the same quarter of 2019. That's an 18 percent increase in sales in Spanish Fort, Daphne and Fairhope. The average sales price was up 6.2%, rising from $326,539 to $347.010. Sellers took on average 2.4% off list price to sell. The average time it took to sell stretched from 42 days to 71 days. Newly built homes accounted for 22 percent of all sales, unchanged from 2019. But new construction represented 34 percent of the homes on the market.

Fairhope: 286 homes with an average price of $433,116 sold this quarter vs. 246 sales with an average price of $407,696 this time last year. Sellers trimmed on average 3.3% off list to sell. Days on market increased from 50 to 79.

Daphne: 329 homes sold compared to 255 sales in the third quarter of 2019. The average sales price increased from $252,463 to $286,665. Sellers took 1.86% less than list to sell. And the time it took to go under contract went from 34 days to 60 days.

Spanish Fort: 137 homes with an average price of $312,171 sold vs. 132 sales with an average price of $318,393 this time last year. Sellers trimmed just 1.07% off list to sell. And the time it took to sell went from 50 days to 80 days.

Real Estate in The Time of the Virus

If you thought that The Virus had an impact on real estate, you’d be right … it’s just probably not what you’d expect.

As of right now, the impact on the housing market in Spanish Fort, Daphne and Fairhope, is negligible.

Home sales are up 19% over this time last year and the average sales price is up 2.4% on the Eastern Shore of Mobile Bay.

And of the 72 listings under contract on April 7 in Spanish Fort, 42 of those homes went under contract in March 2020. Hmmm ….

Some experienced local agents believe the impact has yet to be felt and the timing is tough in that it is the heavy selling season. So I’ll continue to monitor this ….

Meanwhile, the industry is trying to rapidly adjust: There’s a COVID-19 policy for everything from open houses (forbidden) to contract extensions since mortgage loan personnel are working from home (common).

On to the stats:

Eastern Shore: 521 homes sold vs 437 sales in the first quarter last year. Average sales price rose to $319,085 from $310,503 last year. On average, sellers sliced 2.6% less to sell, while they gook 3.1% this time last year. Days on market dropped from 66 last year to 49 days.

New construction, which represented a third of all sales and a $56 million business in the first quarter alone, had an average sales price of $328,711

Fairhope: 190 homes sold with an average sales price of $394,572, compared with 179 sales with an average price of $399,178. This time last year, there were 179 sales with an average price of $370,823. List-to-sale percentage improved from 4.4% last year to 3.3% this year. Average days on market fell from 61 to 44

Daphne: 209 sold vs 161 in the 1st quarter last year. The average sales price rose from $257,309 to $261,870. Sellers trimmed just 2 % of the list price in order to sell -- the same as last year. And the average time it took to sell fell from 66 days to 55 days.

Spanish Fort: 122 homes sold with an average sales price of $299,539; last year there were 97 sales with an average price of $286,333. The list-to-sale percentage dropped from 2.7% to 2%. Days on market dropped from 76 to 49.

PULL IN CASE OF EMERGENCY:

While there are many programs that have been promised to alleviate the financial burden on folks, there may be some who know that their precarious employment/business situation is going to be dire now.

Some may qualify for a short sale of their home. A short sale is when the house is not worth what it owed on it and the owner has a bona fide distress. During the Great Recession I earned my Certified Distressed Property Expert designation to handle these complicated and challenging sales. The benefit to the owner is that the debt on the house is often forgiven and the damage to their credit is less than that of foreclosure.

Housing prices sputter after 2 supercharged years

New developments

Fairhope’s moratorium on new construction is over, but it seems to have led to longer-term consequences.

Of the three Eastern Shore cities, Fairhope, at present, has the lowest percentage of newly built homes for sale.

Here’s the percentage of new construction for sale in each city:

Fairhope: 24%

Daphne: 44%

Spanish Fort: 37%

One interesting bit of data is that construction behemoth DR Horton only has a few listings in one subdivision in Fairhope, leaving that new home market to Truland and some custom builders.

Fairhope did approve a planned unit development (PUD) and annexation request for the northwest corner of Fairhope Avenue and Highway 181. If this project by Gayfer Village Partners comes to fruition, there will be 16 commercial lots, 232 apartments and 67 single-family homes. The Alabama Secretary of State’s office lists Haymes Snedeker as the organizer of Gayfer Village Partners.

In Daphne, plans are under way for Savannah Estates subdivision at the northeast intersection of County Road 54 and County Road 64. A recent revised application that went before the Baldwin County Planning Commission proposed 327 lots on 148 acres.

Market status

If you need to sell, now is your time!

Inventory might be at an historic low on the Eastern Shore, at least so far as recent history is concerned. Houses that are priced right are moving quickly.

Here’s a nugget about the last two house sales in which I was involved: The first received competing offers in its first 72 hours on the market. The second received an offer after just eight hours on the market.

But the flaming hot appreciation of 6% the last two years flat-lined to 0.35% in 2019, even as the number of single-family homes sold increased 11%. The time it took between listing and getting a contract narrowed from 88 to 83 days.

As a colleague of mine said: If home prices kept rising the way they were, none of us would be able to afford to live here. So taking a breather is not always a bad thing.

On to the specific numbers:

For the entire Eastern Shore in 2019, 2,420 homes sold with an average sales price of $308,262. That’s up from 2,165 sales in 2018 with an average price of $307,167. Sellers took 2.8% off list price in order to sell.

In the 4th quarter, 559 homes sold vs. 447 sales at this time in 2018. The average sales price decreased from $310,782 to $300,988. In the 4th quarter, it took on average 75 days to sell. List-to-sell percentage was 2.5%

Spanish Fort: (this 36527 ZIP code includes TimberCreek in Daphne and Stone Bridge in Loxley). 494 homes sold in 2019 with an average price of $293,440, compared with 477 sales with an average price of $295,183 the previous year. It took 86 days to sell and sellers took 2% off the price in order to close.

In the 4th quarter, 109 homes sold vs 97 the prior year. Sales price dropped from $291,440 in 2018 to $275.598. Sellers took 1.8% less in order to sell. Days on market increased from 67 to 81.

Daphne: 676 homes sold with an average price of $241,700. In 2018, 873 homes sold with an average price of $249,884. List-to-sell percentage stood at 1.8%. Days on market rose from 47 to 74.

In the 4th quarter, 240 homes sold compared with 171 sales in that period of 2018. Average sales price dropped to $229,919 from $246,012 the previous year. Days on market rose from 41 to 64 days. But sellers only trimmed 1.6% off list in order to sell.

Fairhope: 924 homes sold with an average price of $391,404. This compares with 815 sales in 2018 with an average price of $375,540. Sellers took 3.9% off list in order to sell, almost the same as the prior year. It took on average 92 days to sell.

What's happening in Spanish Fort, Daphne, Fairhope

Janet English named No. 2 agent at RE/MAX By The Bay

Based on sales numbers, Janet English earned the No. 2 spot at RE/MAX By The Bay, which has offices in Daphne and Fairhope, Ala.

English, who left print journalism to start her real estate career in 1998, is a perennial in the Top 10 at this brokerage. In 2009, she earned induction into the RE/MAX Hall of Fame.

"I love what I do," she said. "I've met so many friends and hope to continue to help folks get to their next destination."

New subdivisions in the works

January, 2019

Twenty years later, Spanish Fort home prices have risen 86%; Fairhope, 103%. (I can’t give you Daphne’s since along the way, Lake Forest was folded into the statistical mix).

I have these pricing figures stored in a stack of newsletters that I’ve been sending to neighbors for the last couple of decades, since I started helping buyers and sellers get to their next destination. The changes over time are truly remarkable.

In 2018, the average sales price for homes on the Eastern Shore, as a whole, reached $307,167, compared to $289,198 in 2017. That marked a 6.2% increase, topping the 6% jump the previous year.

New home construction accounted for 30% of 2018 sales, representing a whopping $206 million worth of property value.

The new construction isn’t likely to slow down any time soon. For example:

n Lots of dirt and dump trucks in the Belforest area of Daphne herald the start of DR Horton’s 900-home Jubilee Plantation project.

n The Bellewood subdivision on County Road 64 on the far eastern edge of what’s considered Daphne has been given a new lease on life after it was purchased by Breland Homes in late 2018.

n A huge new multi-phase development could be on the way to Jimmy Faulkner Drive outside Spanish Fort’s city limits. I was part of a focus group in late 2018 that was asked what amenities should be included in a “Crystal Lagoon” that will be the main attraction in the giant project. Check out the video of a similar lagoon in Florida: https://www.youtube.com/watch?v=NusOclUZcAw

It’s worth your time to see it.

Meanwhile, older neighborhoods are rocking along, too. Housing is moving quickly once the “For Sale” signs go up. For example:

n Sprawling Lake Forest has only 28 active listings, and 20 properties under contract, as of this writing in January 2019.

n The large Spanish Fort Estates has a mere 4 active listings, and 7 properties under contract.

In the words of Huey Lewis and the News: “The future’s so bright, I gotta wear shades.”

But before then, let’s take a look back at 2018. Here’s some of the key sales data for our local area’s specific markets, both for the year as a whole, and for the final quarter of the year.

Eastern Shore overall: In all of 2018, 2,165 homes with an average price of $307,167 sold compared to 2,109 homes with an average price of $289,307 in 2017. Days-on-market dropped to 50 days in 2018, although the formula for deriving that figure was tweaked by the Board of Realtors to represent the time from listing to contract rather than listing to closing. In 2017, it was 127 days. Sellers trimmed 2.7% off their list prices in order to sell, the same as in 2017.

In the 4th quarter, 447 homes sold on the Eastern Shore, compared with 424 in the 4th quarter of 2017. Average sales price dipped to $302,586 from $313,289. But the list-to-sale percentage improved to 3.3% from 3.8%, while days-on-market went to 54 from 99.

Spanish Fort: (This 36527 Zip Code includes some areas in Daphne and Loxley) 477 homes sold in 2018 with an average price of $295,183, up from 438 sales with an average price of $279,440 a year earlier. Sellers took 3% off list price in order to sell; a year earlier, they trimmed the list price only 1.9%. Days-on-market dropped from 146 in 2017 to 61 days in 2018.

In the 4th quarter, 97 homes sold with an average price of $291,440. That was up from 81 sales with an average price of $287,681 in the 4th quarter of 2017. Sellers took 2.8% off list in order to sell, while a year prior they took off 1.8%. Days-on-market went from 101 to 67.

Daphne: 873 homes sold in 2018 compared to 827 homes in 2017. Average sales price rose from $240,430 to $249,884. List-to-sale percentage was little changed from 2.2% in 2017 to 2.1% in 2018. The “Wow!” number was the drop in the time needed to sell: 47 days, compared to 124 days in 2017.

In the 4th quarter, Daphne enjoyed 171 sales, a jump from 157 in the same period of 2017; average sales price stood at $246,012, down from $261,695. In 2017, sellers settled for 3.7% less in order to close; that number dropped to 2.4% in 2018. Days-on-market was again a “Wow!” – It dropped from 111 days to 41.

Fairhope: (This municipality enacted a 9-month building moratorium for certain new construction that ended in September 2017). 815 homes sold in 2018, a decline from the 844 sales in 2017. But sales price rose from $367,992 in 2017 to $375,540 in 2018. In 2017, sellers took 3.4% off list in order to sell; in 2018, they took 3.7%. Days-on-market dropped from 119 to 48 days.

In the 4th quarter, 179 homes sold in Fairhope, compared to 186 in the same quarter in 2017. The average sales price also ticked down slightly: from $367,992 to $362,671. But sellers didn’t trim as much off their list prices in order to sell as a year earlier: 4% vs. 4.4% Days-on-market dropped from 89 to 56 days.

Homes prices continue upward march

October, 2018

Another stellar quarter for home sales on the Eastern Shore with prices up 7.3% compared to this time last year.

The number of single-family homes sold rose 10.6% in Spanish Fort, Daphne and Fairhope compared to the 3rd quarter of 2017.

The cheapest home sold was a cute 480-square-foot cottage in Fairhope that sold for $62,500; the most expensive, a 4,333-square-foot bay front home, also in Fairhope, that went for $2,325,000. The latter was one of six $1 million-plus sales in Fairhope in the 3rd quarter of 2018.

Before we get to the numbers: The Baldwin County Association of Realtors’ multiple listing service website has changed the way days on market (DOM) are calculated. Previously, this numbers started the day the property was listed and ended the day it was closed. Now, it freezes upon accepted offer time when the property is put in as a pending sale.

However, the time it takes to sell -- start to finish -- is shrinking.

On to the numbers;

Eastern Shore: 594 single-family homes sold, with an average price of $300,778. In the 3rd quarter of 2017, 537 homes sold with an average price of $280,216. Sellers settled for 2.6% less than list price in order to sell. Homes were actively marketed on average 43 days before going under contract.

Fairhope: 214 homes sold with an average price of $367,421 (very much skewed by the $1 million-plus sales). This time last year, 205 homes sold with an average price of $327,510. Sellers took 3.6% off list price in order to sell. Days on market stood at 46 days.

Daphne: 255 homes sold, compared to 224 sales this time last year. Average sales price rose to $250,620 from $239,013 in the 3rd quarter of 2017. Sellers trimmed 1.9% off list price in order to make a deal. It took on average 35 days from list to contract.

Spanish Fort: 124 homes sold with an average price of $300,778. This compares to 108 sales with an average price of $275,905 this time last year. Sellers settled for 2% less in order to sell. And days on market stood at 54.

Market swings to favor sellers

June, 2018

Home sales on the Eastern Shore are cruising ahead, keeping pace with this time last year almost exactly. With a notable exception: The average sales price is up 7.3%! That’s a large indictor of a market that is steadily tightening in the sellers’ favor.

And here are two other pieces of interesting data from the recently completed second quarter:

* New homes represented 32% of all sales in Spanish Fort, Daphne and Fairhope.

* The time it took to sell – “days-on-market” -- dropped to under three months, from more than four months at the same time in 2017.

This year, the reporting of days-on-market freezes at the point that a house goes under contract, eliminating the closing or escrow period. Still, this drop is certainly eye-catching.

Let’s look at the compete sales numbers for the second quarter of 2018 on the Eastern Shore:

Eastern Shore as a whole: 670 single-family homes sold with an average sales price of $311,033, compared to 671 sales with an average price of $289,893 during the second quarter of 2017. Sellers trimmed an average of 2.3% off the asking price. And days-on-market tumbled to 88 days from 135 days.

Spanish Fort: 146 homes sold, compared to 147 sales in the same period last year. But the average sales price (largely fueled by new construction in this ZIP code) jumped to $301,087 from $282,679. On average, sellers took 1.55% off their asking price. (This number is very likely affected by new construction where few discounts are given). Days-on-market dropped to 94 days from 148 days.

Daphne: 283 homes sold, up from 261 sales this time last year. Average sales price also jumped, to $265,466 from $237,341. Sellers settled for 2.2% less than list price. And the time it took to sell dropped to 91 days from 134.

Fairhope: 241 homes sold, down from 263 sales in the second quarter of 2017. But the average sales price rose to $377,430 from $346,115. Sellers trimmed 2.9% off list in order to close. Days-on-market was the Eastern Shore’s shortest: 81. That figure was 125 days at this time last year.

March 30, 2012

You can't judge a school system just by its test scores, but it sure is a good place to start.

So check out the Alabama State Department of Education's Accountability Reporting System.

Pick the school you'd like to research and then you'll have an option of choosing from 4 Alabama test reports, including the High School Graduation Exam, and the Stanford Achievement Test.

If you want to get my take on the school system from a veteran parent, just give me a call at 251 591-2411 --- Janet

Jan. 30, 2012

If the Eastern Shore is where Mayberry meets Maguaritaville, then Cheryl's Cafe is pure Mayberry, where regulars are greeted by name and non-regulars are soon to find something so addictive on the menu that they join the following.

Unauspcious at the end of a small strip of shops at U.S. 98 and Hwy. 31 in Spanish Fort, Cheryl's offers a a variety of fresh sandwiches and sides, as well as a heartier host of specials that change each day. Get there too late and you may watch as your favorite is wiped off the board.

small strip of shops at U.S. 98 and Hwy. 31 in Spanish Fort, Cheryl's offers a a variety of fresh sandwiches and sides, as well as a heartier host of specials that change each day. Get there too late and you may watch as your favorite is wiped off the board.

What it all comes down to is that Cheryl is a very good cook, who has compiled a few secrets that simply enhance a standard dish.

So here are some of my favorites from the printed menu:

Chinese Chicken Salad: Ramen noodles are toasted and tossed with sheddred cabbage, lean chicken, water chestnuts, scallions, sesame seeds and an oil-and-vinegar dressing.

Chicken Salad: Maybe best around. Light and refreshing with mayo and crushed pineapple (yes, Cheryl has revealed a few of her secrets over the years).

Club Sandwich: Easily feeding two, everything is fresh here from the Boar's Head meats to the tomatoes. This sandwich is so thick every bite's a challenge.

Mitch's Reuben: My father's favorite, with tender, lean corned beef piled high, kraut and Thousand Island dressing on rye.

Sides are pasta salad, fresh fruit, cole slaw or potato salad, all freshly prepared.

From the day's menu, you may find pot roast or chicken and dumplings, shrimp salad or crawfish bisque. Any one of these will please and you can pick from about a dozen vegetables to round out your meal.

Some of my favorites:

Taco salad, with fresh greens, taco meat, beans, avocado, cheese and chips topped with a sort of salsa/Thousand Island dressing.

Tender pot roast with sweet green beans and a to-die-for yellow squash casserole. Cheryl has shared the secret to the green beans, but I shouldn't give everything away.

Service is quick and efficient. So this is often where I stop for lunch with buyers looking for real estate in Spanish Fort or Daphne.

It's snug at Cheryl's with barely enough room to maneuver between the red-and-white checked tablecloths, so this is not the place for intimate conversations.

Prices are moderate.

Address: 6580-D Spanish Fort, Blvd.

Phone: 251-626-2602

Jan. 30, 2012

Perhaps there's no better way to view Daphne's history and beauty than a brisk walk through Village Pointe Park Preserve, off Scenic 98.

Evidence of Indians, Spanish, French and English settlers has been found in the park, and while you won't see historic replicas of these forebears, you will see the land they were attracted by.

Rich with native trees, streams, tidal pools and wetlands, Village Pointe can be explored on foot or bike. Walk the dog or grab your fishing pool or towel because at the end you'll find a fishing pier and beach with panoramic views of Mobile Bay.

A brisk 20 minute walk past cypress knee swamps, deep forests to your final destination. Stop midway to view the Jackson Oak, some 95 feet tall and 28 feet in circumference, believed to be where Gen. Andrew Jackson addressed his troops in the War of 1812. According to the park site, the oak was shown on a survey in the original Spanish Land Grant map of 1787.

Even though I know this area well, it's still a wonder to emerge through the woods and find the beach.

Oct. 6, 2011

Freddie Mac announced Thursday that 30-year fixed mortgage rates fell below 4% for the first time ever. The new rate - just 3.94% - is lower than the rate in the 1950s, according to the National Bureau of Economic Research. For buyers looking at homes in Daphne, Fairhope and Spanish Fort, you'll find the 15-year fixed rate in the lower 3% range locally.

For example, Mary Brabner, loan originator for Region's Mortgage in Daphne, AL, says her 30-year fixed rate is 3.875% today. This is for over buyers with credit scores over 740, with 20% down on a purchase. A 15-year rate is 3.25%, Brabner said. Dean Watson of WestStar Mortgage, also in Daphne, AL, says rates may be higher for those whose credit scores are below 740. WestStar offers mortgages that don't require the often pricey wind coverage for home owners insurance; for that the rate may be a bit higher, he said.

With a nice selection of homes for sale in Spanish Fort, Daphne and Fairhope, it's a great time to buy and lock in a low fixed rate. If you have sufficient equity, it's also a great time to re-finance.

Oct. 5, 2011

Veterans closing mortgage loans after Oct. 1, 2011 will find that the funding fee has been reduced on VA loans.

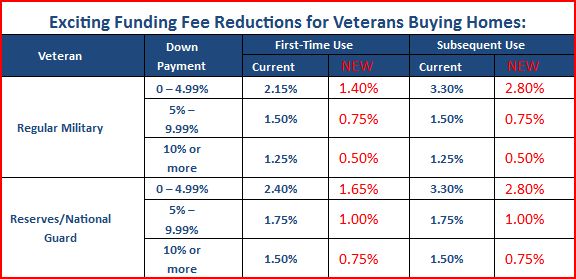

Here's the new structure:

VA loans may not always be the best choice for financing, so be sure to do your research.

Oct. 5, 2011

What is a short sale?

A short sale is the sale of a home or property for less than what is owed on the property. The seller must have also experienced some sort of “distress” and must sell. (Example, the seller of a home in Daphne AL owes $250,000 and the house value has fallen and it’s only worth $200,000. So there is an immediate $50,000 shortfall plus closing costs). It does not necessarily mean that the property is heading into foreclosure.

Why is it sometimes called a potential short sale?

That’s because it is ultimately up to the seller’s lender to approve the sale. After all, it’s the lender who is taking the major financial hit here.

What qualifies as a distress for a seller?

Many, many things from personal to financial misfortunes, to simple changes in circumstances. One lender even has a checklist. Death, divorce, illness, expanding family, loss of job, reduction in pay or hours, even increased home owners’ insurance payments. Many short sellers have experienced a combination of one of more of these.

Can anybody who has had a change in circumstances qualify for a short sale?

No. The seller cannot have a lot of cash available, no substantial assets. Basically a seller can have just enough to get by.

Who sets the price?

The Realtor sets the price according to the market value. When there aren't a lot of comparable solds to determine price, the Realtor may start the pricing at what is owed on the property then systematically reduce it over time to demonstrate to the lender that the house wasn't being shown at the higher price and the market value has declined.

How long does it take?

Short sales used to have a reputation for being a nightmarishly long experience. But over the years the time it takes has been reduced to around 45 to 90 days.

Is it really better for the seller to do a short sale or to just let it go into foreclosure?

The general school of thought is that a foreclosure will result in a larger hit to a credit score than a short sale. The same holds true for deed in lieu of foreclosures (where you give the house back to the bank). This is because foreclosures are recorded at the courthouse and end up on your credit. Short sales typically are not. Also, a short seller should be able to purchase a home again within a shorter period of time than someone who has been foreclosed upon.

Does a seller have to pay anything in a short sale?

It depends. The lender can file a request that the seller repay all or part of the difference between the sales price and what is owed. In my experience I have seen the lenders forgive the debt entirely, and I have seen then lender write off around $100,000 and request the seller repay just $2,500 over a period of years with payments under $100 a month.

So what does a seller have to do to get a short sale going?

A qualified Realtor can guide a seller through the short sale process. Generally, the lender will request the seller write a letter outlining their personal, work and financial history and why they are requesting a short sale. The lender will also request copies of bank statements, pay stubs, and tax records.

Sounds like a lot of work?

Yes, it's some for the seller, but even more for the Realtor who has the house listed. But it's an good option for homeowners in financial distress who need to move.

If I've received a default notice is it too late to do a short sale?

It depends on where you are in the foreclosure process and whether you meet the short sale criteria.

Do I have to be late on my mortgage payments to qualify for a short sale?

I cannot tell you to not make a mortgage payment, but the general school of thought is you have to be late or make a partial payment for a lender to consider a short sale. I have heard of one lender that doesn’t require you to be behind on payments to do a short sale. But be careful here: If you are late too many months, you will trigger the big, bad foreclosure process which can complicate the short sale.

If you think you may qualify for a short sale and need more information, feel free to call me at 251 591-2411.

Aug. 30, 2011

"Would your sellers consider a lease purchase?" two separate agents have asked me in the last two days on two separate listings.

And each time, I've explained the pros and cons of such an arrangement to my sellers. Both sellers passed and here's why.

First, the Wikepedia Definition: "A lease purchase contract is a shortened name for lease with option to purchase contract. It is a form of real estate purchase which combines elements of a traditional rental agreement with an exclusive option of right of first refusal to later purchase a home."

The initial challenge of a lease purchase is to make sure everyone knows what they are talking about, even the agents. Often, the buyer is thinking "lease with option to purchase" while the seller is hearing "purchase with delayed closing."

This hybridized contract has come and gone over the years, most recently with the soaring interest rates in the ‘80s, and now with the difficult market we face today. It's a product of desperation, really no better than simply renting a house. In the end, it's like like trading in house futures.

Here's a typical scenario:

Mr. Buyer has a home on the market in another city. But his job - and the kids' school - starts in your market in one month. He wants to get his family settled. He's found the perfect house for $200,000.

Mr. Seller is thinking about building a $300,000 house and has his house on the market. It's a slow market, a soft market and maybe he'll get full price if he agrees to this lease purchase. Mr. Buyer comes along with the lease purchase proposal. Ms. Seller thinks he can rent elsewhere and get started building his new house. The agents negotiate the offer - one part lease and one part purchase -- with Mr. Buyer providing $10,000 non-refundable earnest money if he doesn't close within the year. (In some cases, Mr. Buyer will want a portion of his "rent" applied to the purchase price.)

If you can get past the obstacle of Mr. Buyer agreeing to non-refundable earnest money, then on to the more mundane home inspection issues, here's what the principals and agents could encounter.

Benefits to seller:

- Possibly higher selling price.

- Cash flow, particularly if property is vacant (which is why this may be attractive to some builders.)

- House is under contract (maybe or maybe not)

Cons for seller:

- Equity still tied up in house and seller cannot proceed with his plans to buy, etc.

- Housing prices could rise and the seller is locked into a lower purchase price.

- Market could decline and tenant/purchaser decides house is not worth agreed upon price. Or tenant/purchaser may find another house they like better in the interim.

- Interest rates could rise and tenant/purchase may not qualify for a loan.

- Tenant/purchaser may not keep up property.

Benefits to buyer:

- Making only one move saves time and money vs. renting, buying and moving again.

- Buyer gets to shakedown period to really figure out if they want to buy this property.

- Housing prices could rise and tenant/purchaser now finds he's made a pretty good deal.

Cons for buyer:

- Locked into agreement and they decide house is not worth price or find another property.

- Interest rates could rise and tenant/purchaser sees his payment going up when the house closes.

Money always talks and in this case it's the $10,000 non-refundable earnest money that's keeping this deal together.

The longer the terms of the contract, the more likely that housing and financial markets will change, making what once seemed like a good deal, merely a memory.

For agents, it's a lot of work with little promise that the house will close. Chances are, no one will be happy. Not the buyer. Not the seller and certainly not the agents.